Assessing the investment climate for new generation and storage capacity

There are countless forecasts from a broad spectrum of analysts that the recent trend in development

of renewable generation will continue indefinitely into the future. Such forecasts from financial

institutions, governments, and independent research organizations are based on the same drivers as in

the past several years: cheaper inputs, more efficient technology, and ongoing government incentives

to further reduce greenhouse gas emissions associated with power generation. And with nuclear

generation facing a constant headwind despite its lack of greenhouse gas emissions, consensus forecasts

show continued steady penetration of wind and, especially, solar generation in most developed

countries as well many important developing regions. Cheaper battery storage and its potential to

alleviate intermittency provide further underpinning for renewables deployment.

To the extent there are differences in outlooks for power infrastructure development, they tend to focus

on the shorter-term impact of the pandemic on procurement and construction and on the longer-term

political environment given upcoming U.S. elections potential government stimulus programs. By

contrast, there is relatively little attention paid to the life blood of development: availability of

investment capital. All forecasts tend to assume that the financial terms on which development has

occurred to date will continue into the future; in other words, without significant constraint.

This may be a safe assumption. But, like most other aspects of long-term forecasting, it’s really just an

informed guess. We can’t refute it, but perhaps we can understand it better by identifying the various

stages of development – including construction, operation and integration with other assets – and the

financing requirements associated with those stages. A substantial portion of development capital is

provided by private sources, making assessments somewhat subjective. But there is information from

public markets – equities, debt, and commodities – that one can utilize to aid in the analysis.

We are not attempting to present a quantitative assessment or another forecast of growth rates. As in

other industries and even within the power sector, the rate of change is accelerating and adding greater

complexity to financial modeling. We are simply trying to gauge the investment climate with greater

specificity and conclude that financial conditions are indeed supportive in most of the relevant areas.

Ultimately, though, financing is only assured when a significant portion of forward revenues can be fixed

at predefined hurdle rates. Long-term power prices have been holding up – indeed rising – in recent

months. If they were to weaken in the future the investment climate would almost certainly degrade.

Capital costs are low, but it’s not that simple

There is one easy way to summarize the main questions posed above and to keep this discussion brief:

There isn’t any financing constraint in a world of zero or negative interest rates. Ultra-low interest rates

are fueling liquidity and higher equity valuations across almost all capital-intensive industries, beyond

utilities and independent power producers – with the exception of oil producers and refiners.

Moreover, in a pandemic-inflicted economy in which central banks have further eased monetary policy

and governments provided fiscal stimulus, policymakers and interest groups are calling for additional

investment in the energy transition toward electric power, an industry seen as a significant job-creator

in the decades ahead. Financial institutions tout the resources they are devoting to the cause.

Even without direct or indirect government support, there is a widespread expectation that the shift

toward low-or no-carbon energy supply will be facilitated by financial commitments from traditional

institutional investors. A casual assessment of investor preferences over the past couple of years from

public equities displays a clear shift away from traditional energy suppliers – primarily oil and gas

producers, refiners, and processors – toward those that are associated with renewable power. The

chart below compares the XLE index of traditional oil and gas companies (in blue) with the Invesco Clean

Energy ETF (orange), which includes solar manufacturers and developers of renewable energy and

battery storage.

Low interest rates and a shift in investor preferences for sustainability provide a powerful combination

for relatively easy financial conditions. Nevertheless, some analysts have cautioned that sharp decline in

public utilities’ equity valuations and widening of credit spreads during Q120 and early Q220 could put a

dent in longer-term growth expectations. Others see pandemic-related economic contraction as likely

to limit corporate profit and associated tax liabilities which could, in turn, could lessen the availability

capital from a particular source: tax equity investors. But much of the disruption in public equity and

debt markets turned out to have been temporary as financial conditions improved in late Q220 and

Q320 and, with U.S. corporate earnings holding up better than expected earlier this year, tax equity

availability may also prove to be relatively abundant.

Still, it would be overly simplistic to assume the financial picture is uniformly supportive. There is plenty

of complexity involved in evaluating financial conditions of the power sector as there are many distinct

roles played by regulated utilities, unregulated generation subsidiaries, and early-and late-stage

developers of both generation and storage assets. Separating these subsectors isn’t easy, in part

because the larger enterprises straddle several of them, and forecasts of investment and operations

tend to get lumped together. Understanding how capital costs factor into development requires

focusing on those companies that specialize in new equipment as well as on the relevant portions of the

more diversified companies.

The standard Wall Street analyst covering the power sector tends to reach far and wide – generalists

that cover a range of participants from regulated utilities to specialized equipment manufacturers.

Independent research firms may carve out specific areas of coverage such as regulation, grid operations,

or new technology. The power industry is diverse and, given its size, supports a plethora of coverage.

Putting it all in perspective – from the point of view of an investor – takes effort.

Among the companies involved, utilities can be relatively pure-play distributors of power with an old-

fashioned business model operating in a heavily regulated market whose investments and returns are

subject to public allowance. Or they can be more progressive and own capacity that is subject to

wholesale market pricing outside of their distribution network. They can own transportation and

storage assets that are typically associated with trading companies. And they can enter into marketing

businesses outside their home region, selling power produced by other companies to retail customers

on the basis of price and customer service. Utilities can do some of these things, or all of these things.

And they can do a portion of them from within their regulated businesses or in unregulated subsidiaries.

And then there is development: investing in new generation capacity to alter their assets’ efficiency and

carbon footprint as well as to take advantage of perceived market opportunities. They can invest at

early stage and take on all of the associated permitting and construction risk, or they can focus on

buying such assets only when they are nearing completion. Some companies are better at early stage

investing while others focus more on operations.

In our view, existing coverage of the power industry doesn’t break these distinctions down very easily.

Analysts don’t clearly distinguish the conditions at any given time that might benefit one area of focus

over another. So, in our attempt to shed some light here we break the industry down into distinct

subsectors that share similar characteristics. 1) regulated utilities, i.e. those involved primarily in

distribution of rate-regulated power and natural gas; 2) their unregulated subsidiaries, which mostly

generate power, either for their regulated subsidiaries or, more likely, for others in the marketplace;

and, 3) early-stage developers of new generation (and storage) resources.

Regulated utilities are among the most traditional of public equity issuers. Their shares, based largely on

the predictable income of their regulated power-distribution business, comprise a significant portion of

the portfolios of private and institutional investors and have been considered among the most defensive

sectors. At its core, the regulated utility business is a tolling business that tends to have predictable

results based on gradual changes in demand and guarantees on the performance of investment in new

capacity. Dividends are steady as long as the economy behaves somewhat normally.

In general, sharp contractions in demand – such as from the global pandemic – have adverse impacts on

regulated utility valuations because they are a volume-based business. Like any tolling operation, a

decline in the volume of flow through their system has a proportional and direct impact on revenue.

Aside from fuel inputs, costs tend to be more fixed.

Regulated utilities may own unregulated subsidiaries and, indeed, renewable generation – making

comparisons among these companies more difficult than if they were limited to only one category. But,

in general, the regulated portion of these companies is the most significant value driver. In 2020,

indexes that track the industry have generally lagged the rebound in the broader equity markets since

last spring, reflecting the pandemic-related decline in power demand that continues to this day. Given

the singular purpose of regulated utility, there hasn’t been any countervailing improvement elsewhere

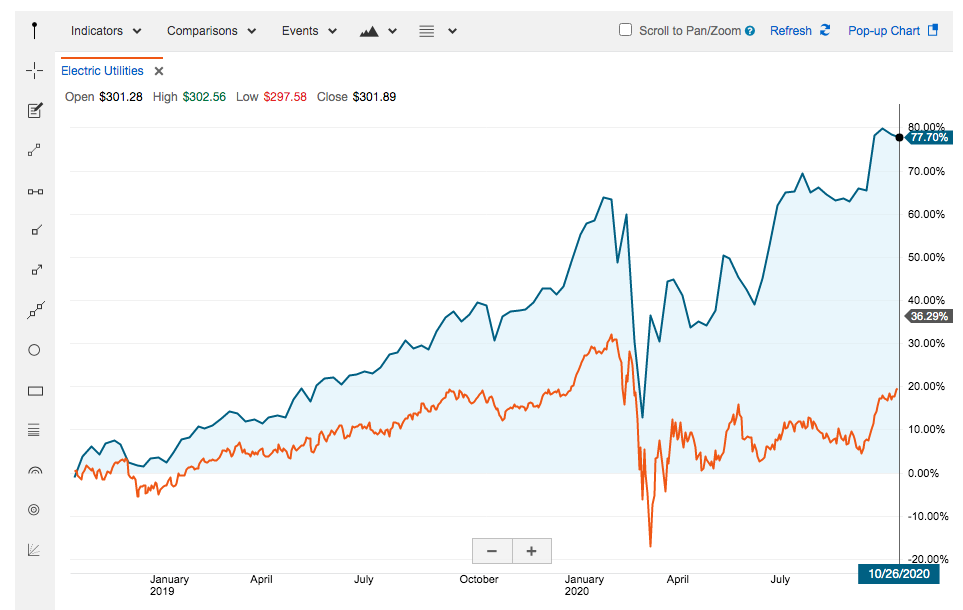

in their business. The chart below compares the S&P 500 utilities index (white) with the broader S&P

500 index over the past year.

Even with lower power demand and relatively fixed capacity, electric utilities are on relatively sound

financial footing, including those with unregulated subsidiaries. It doesn’t matter so much whether their

unregulated business tends to focus on early-stage investment in new generation or whether they are

purely operating companies. Should they seek to invest in additional generation there is ample equity

and debt capacity available. If anything, those with more aggressive renewable generation expansion

plans tend to have easier financial conditions. There is perhaps no better example of this than NextEra

Energy Inc. (turquoise in chart below, vs. broader electric power utility index in orange), which has a

sizeable regulated business but also the largest renewable portfolio in the U.S.

It is perhaps worth noting that a number of large European utilities have been making significant inroads

to the U.S. market over the past several years, based in part on their expertise in renewable power

development and asset operations. These companies comprise a significant portion of the expected

ownership of future renewable resources in the U.S., especially in offshore wind where their expertise is

most advanced on a relative basis. European governments provide financial backing for most of these

utility companies, keeping their financing costs comparatively low. Indeed, while U.S. companies tend

to utilize project financing for building new assets, European utilities generally borrow against their

balance sheet. Given those governments’ commitment to driving future growth in renewable power,

there is good reason to expect financial conditions to remain conducive.

Unregulated generators, independent power producers, and yieldcos

Unregulated independent power producers (IPPs) own generation assets and sell their output into

wholesale power markets, but aren’t in the tolling distribution business of regulated utilities and don’t

have the steady income that such business provides. Their financial performance is more volatile than

that of regulated utilities but can be managed with greater focus on consistency. Broad trends in

demand and supply for power can be forecast with a fair degree of precision over the life of their assets,

but commodity prices nevertheless need to be hedged.

This industry has experienced periods of far less stable financial performance and surely has been

stressed – especially when natural gas – the marginal power input in most markets – has been in cyclical

downturns. Low gas prices drive power prices down and margins can suffer while fixed costs take on

greater significance. Independent power producers tend to be relatively leveraged given their capital

intensiveness; this can be problematic amidst persistently low commodity prices.

IPPs can be owned by private equity or as standalone public corporations (e.g. Vistra Energy). They can

also be housed within utility holding companies. In addition to their generation business, IPPs can own

retail marketing divisions, which is different from the tolling business of providing delivery of power.

Retail marketing allows generators to sell power at retail prices which they can set according to open

markets, delivered to their customers via local utilities.

If IPPs are adequately hedged then their returns can be predicted with greater confidence and their

equity can be marketed to investors as steady yield providers (aka yieldcos). Their generation can be

incorporate varying degrees of renewable resources but, importantly, they do not develop new

resources given the higher risk factors associated with early stage development. They purchase

generation assets once they have been built by other – sometimes related – companies that are more

focused on securing permits, materials, engineering, and construction.

This year has obviously been different and IPPs are not only exposed to pandemic-related volume

declines but also to price declines where hedges either don’t exist or are less effective. As a result, IPP

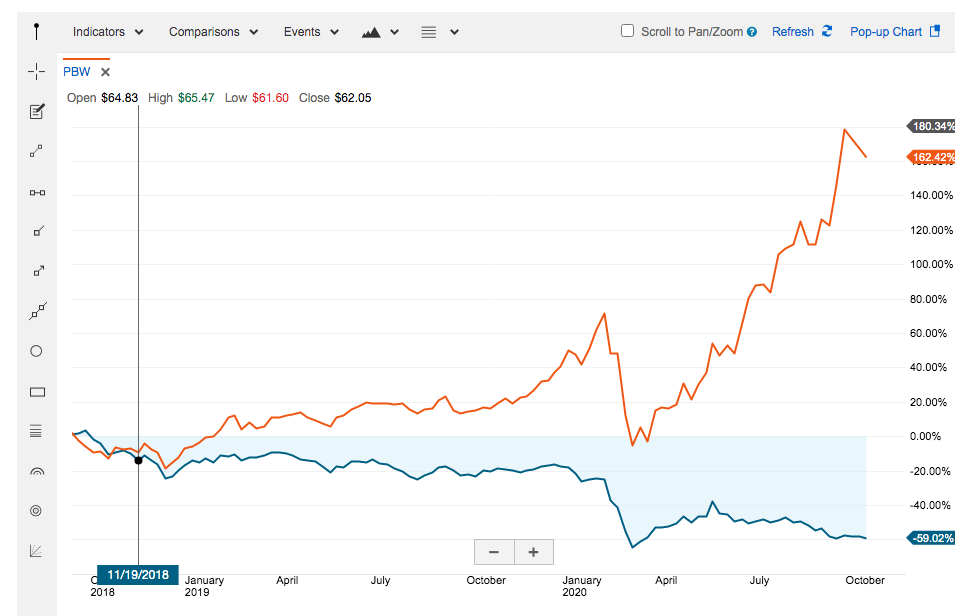

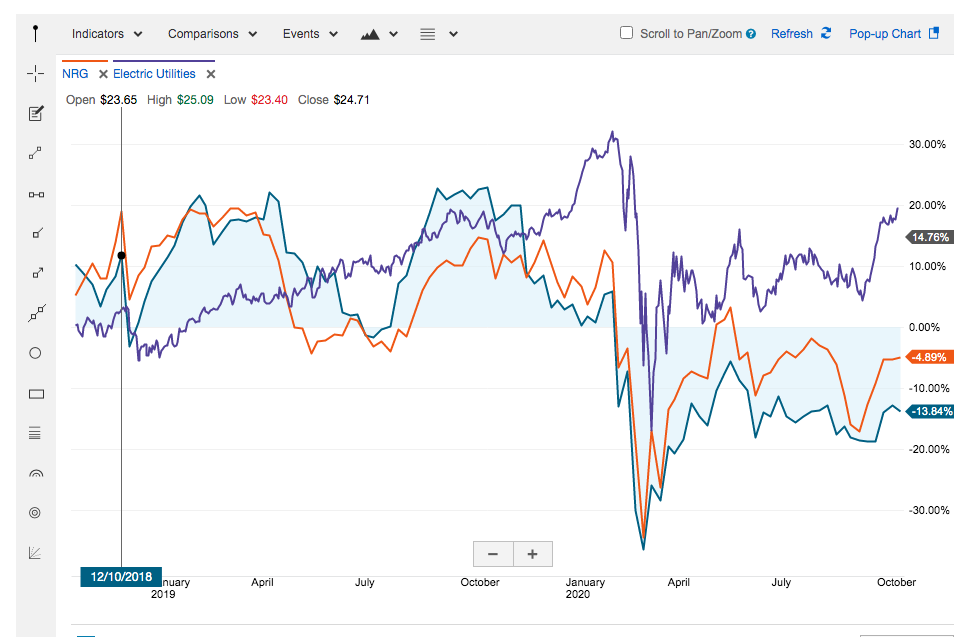

equity valuations have underperformed this year. The chart below shows two of the larger IPP names:

Vistra (turquoise) and NRG (orange) vs. a broader electric utility index (purple).

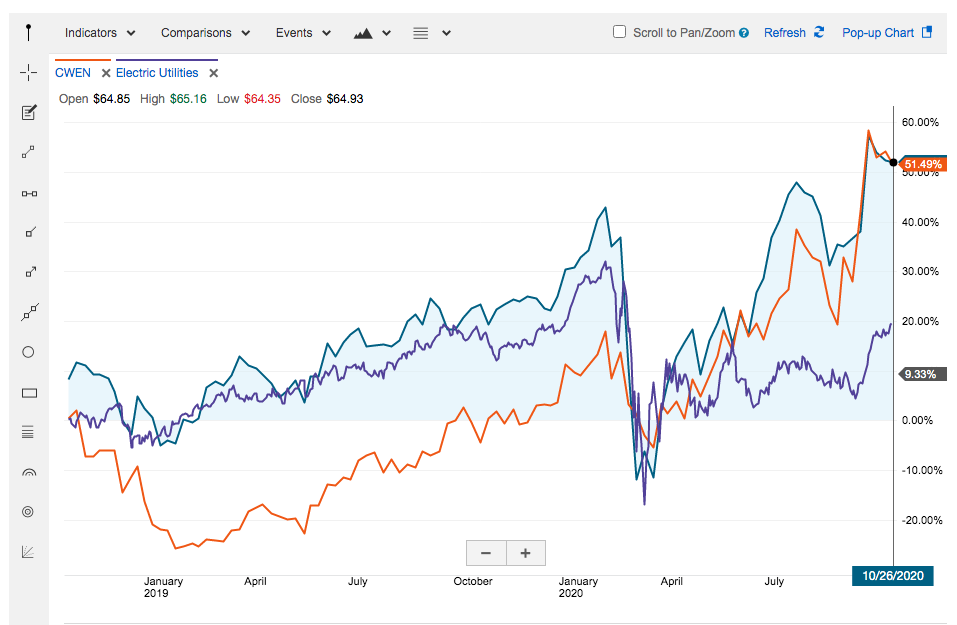

The equity market’s relative distaste for IPPs does not, however, extend to those that are focused on

renewable generation. The chart below shows the relative performance of two of the larger

renewables-focused yieldcos, NextEra Energy Partners (turquoise) and Clearway Energy (orange) vs. the

same electric utility index (purple) in the chart above. Given recent investor interest in this particular

group of companies, it is fairly clear that the financing climate is supportive. A key consideration here is

the predictability of the yield which, in turn, depends power prices being relatively fixed, either via longterm

price agreements or via financial hedges. We discuss these markets in our conclusion below.

Early-stage developers, focused primarily on renewables

Regulated utilities, IPPs and associated yieldcos tend to be public companies with ample analyst

coverage. But turning our attention to developers is more of a challenge. On the one hand, there are a

handful of public companies involved in developing distributed

power; i.e. those that build and service

solar power systems among residences and small businesses, housing projects, etc. There are also a

number of public companies that manufacture the hardware and software that these systems require.

On the other hand, those involved in developing early-stage utility-scale generating assets – whether

renewable or natural gas-fired – tend to be owned by private equity and thus much less transparent

analysts of the public markets. We address each of these sub-sectors below.

Companies involved in distributed generation suffered some setbacks earlier this year as customers

slowed their purchases and procurement also suffered from constraints on manufacturing and

transportation of components. Subsequently, however, orders picked up sharply and most companies

are pointing toward further growth in 2021. Financing for this sector has perhaps been as easy as

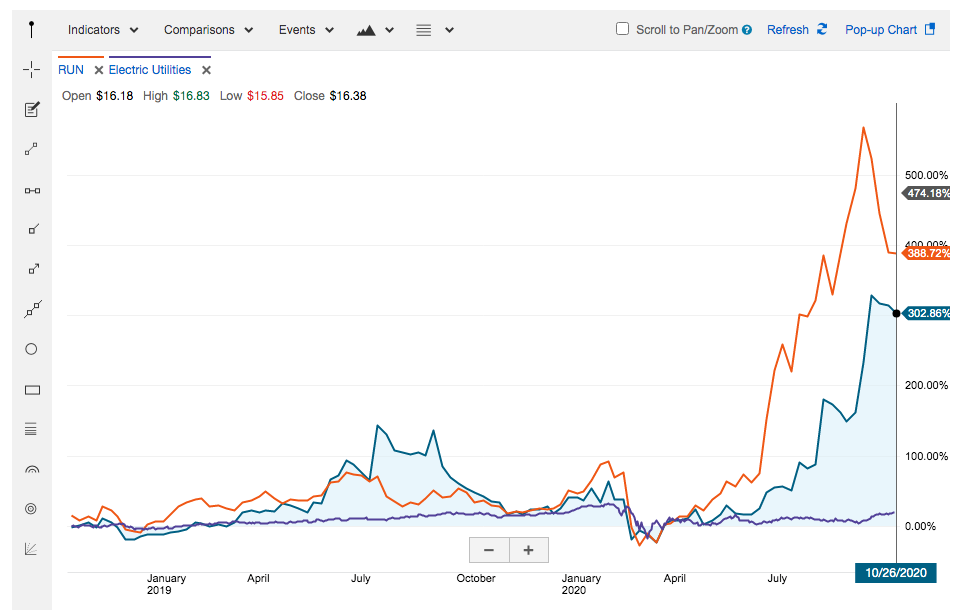

anywhere else given the extraordinary run of equity prices since March. Sunrun is the bellwether

company in the space but its peers also show similar rebounds to reach all-time high valuations recently.

The chart below shows Sunrun (orange) and SunPower (turquoise) vs. the broader electric utility index.

Turning toward utility-scale developers we enter the realm of private equity which has long had a

significant role in financing independent power development including natural gas plants, wind farms

and, increasingly, solar assets and battery storage. Regardless of the technology, early-stage investors

are willing to take on considerable risk of land acquisition, permitting and construction. Once built,

utility-scale assets are then typically sold to utilities or IPPs (public or private).

One might question the distinction between early-stage development and later-stage operations and

why some companies tend to be on one side but not the other. The best justification is the risk involved

in development and the higher cost of capital involved in that early stage of a project’s life. The

operational stage of a project introduces the opportunity for the developer to monetize their

investment and move on to the next opportunity. The buyer is likely to have access to cheaper capital –

in large measure due to the lower risk and greater diversification of their business – and to utilize that

capital more efficiently via leverage. In this sense, developers are like the early-stage exploration

companies in oil and gas production. They have high capital cost but superior expertise. Once they

prove out the value of a speculative asset, they can sell it at a higher multiple to an enterprise that can

manage it effectively with leverage and a lower cost of capital.

There is another parallel here to the oil and gas industry: early-stage development and later-stage

operation can also be housed together among larger companies. In the power sector, those firms are

the large, diversified utilities while in oil and gas it is the integrated companies and some of the larger

independent producers. We have already addressed the generally friendly financial conditions in which

large utilities currently operate. But what about the small, privately-owned developers? How can one

assess the investment climate today in this very focused industry? The answer warrants a brief detour

to address an important component of financing: tax credits.

Tax credits are a significant driver of availability of capital to the development and operation of

renewable generation assets. It is true that the financial performance of the industry has improved with

steady declines in costs, but there is still an important component that comes from federal tax

treatment: investment and production tax credits.

U.S. tax law grants credits to investors in wind and solar power development. These are available in

two forms: the investment tax credit (ITC) and production tax credit (PTC). The ITC is the simpler of the

two and applies to solar installations: it allows a straight tax credit equal to 26% of the cost of the solar

installation in the year in which construction takes place. The ITC is not a permanent feature of the tax

code and has already begun to be phased out. It was previously 30% and will decline to 10% by 2022

(and disappear entirely for residential systems) if it is not extended by law.

The PTC is a bit more complicated and applies to wind power and other qualifying renewable sources.

The PTC also grants tax credits to owners of these assets but the credit is variable, based on the amount

of power generated (at a $/kWh rate of as much as $0.025) for 10 years. There are other complicating

features, including a cap on power prices that would reduce it if reached and other limitations

associated with alternative minimum tax. Like the ITC, the PTC is also temporary. Its phase-out is more

abrupt, however, disappearing entirely at the end of this year unless extended by law. Given multiple

extensions in the past, it could continue for years into the future.

Both the ITC and PTC have been instrumental to the development of the U.S. renewable power industry.

In broad terms, those credits have a cash value equal to as much as 30% of the investment cost or

expected revenue of a project. As such, they are certainly material to expected returns. This tax benefit

spawned an industry catering to identifying investors with appropriate tax liabilities and guiding them

through the process of investing and applying the credits to their existing portfolio or operating

businesses. Tax equity investing is often at the forefront of discussions about the future financing needs

of renewable power developers.

Any changes to tax law – whether by extension of credits or their ultimate phasing out – will affect all

investors in renewable projects. There are plenty of large utilities that take advantage of the credits by

applying them to the tax liabilities in their profit-generating businesses. Those companies may need to

apply less of a benefit in the future and, in some cases, already are doing so. To date, however, there

doesn’t seem to be any real evidence of a pullback in investment. If anything, utilities that invest in new

renewable capacity are accelerating their investment plans while the credits are still available.

Arguably, a disproportional impact of credits phasing out will fall on those developers that depend on

external financing. Unlike diversified utilities, these smaller companies that focus exclusively on project

investment do not have other operating businesses against which to apply credits. Among their

investors, weaker earnings and lower corporate tax rates, especially since the U.S. federal tax reform in

2017, reduce their liability, in turn, lowering their need to seek offsetting tax credits.

Recently, there have been some rumblings from the developer community that capital availability is

more limited. Although other aspects of development such as declining costs for solar panels or battery

storage may strengthen project economics, the investor pool will require higher returns if there isn’t

enough tax liability to take advantage of the credit. Ultimately, the industry will have to stand on its

own merits, competing for private and public equity capital on a level playing field with other asset

developers. The issue for the next few years will be bridging the gap between a historical reliance on tax

benefits and a future without them.

Our quick summary of equity capital markets is one of ample availability – certainly for the larger

utilities and independent power producers with a stable of operating assets. But there is also little

evidence of constrained resources available to smaller developers focused on early-stage investment. If

there is any evident constraint, it is in the tier of asset owners that depend on tax equity funding and

could be subject to declining contributions from that specific source. This would be especially likely if

there were no additional extensions of either the ITC or PTC programs. There is nevertheless a

possibility that other sources of private equity capital could be deployed into this space if the returns are

sufficiently attractive. Private equity firms do not seem to have much difficulty raising funds, even in the

current pandemic-dominated environment, and lower expected returns in some other sectors could

drive new pockets of capital toward electric power infrastructure projects.

Debt financing considerations

Debt markets are also relevant to this discussion. As in other energy investments, including oil and gas

exploration and production, capital structures change over the life cycle of assets. Early-stage

development tends to start with the least leverage as the potential outcomes are at their most variable.

As development is completed and assets move into the operation phase, owners can increase leverage

with greater confidence that the expected volumes will be produced. They can gain further confidence

by hedging the unit price of the output via fixed-price physical sales or via financial derivatives.

As with equity, we can get a sense of debt capital availability by examining the yields of instruments

trading in the public markets – mostly issued by utilities. Comparisons based on credit spreads are far

from perfect, as many utilities are purely tolling businesses without any commodity price risk while

others may have more significant wholesale generation that can have significant commodity price

exposure. If there were any significant disruption in the market for utility bonds, there would certainly

be negative implications for any debt owed by IPPs and other companies with more of a focus on

renewable power generation.

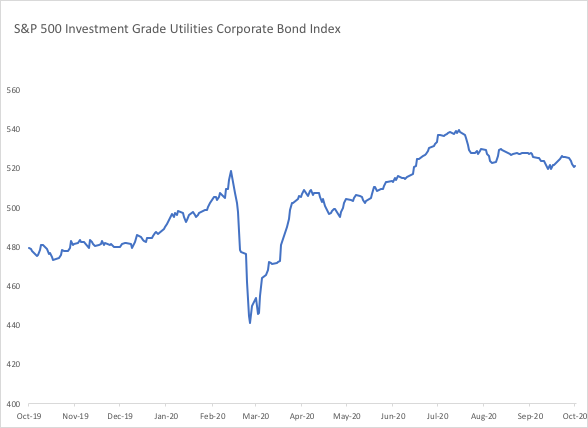

Credit spreads on utility bonds rose during the most volatile market turmoil of Q120. But as with most

other sectors, credit spreads quickly tightened again across the utility space as it became clearer that

demand would recover in all but the commercial sector. The chart below shows the change in value for

the benchmark S&P Utilities bond index. Current values are similar to pre-pandemic levels.

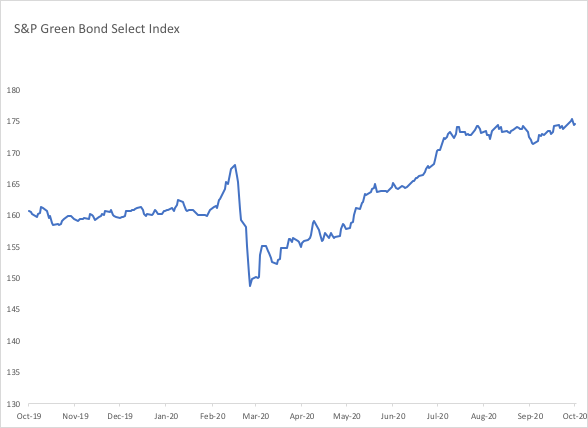

As a reflection of the equity market’s superior valuation for companies involved in renewable power

generation, indices that track so-called green bonds have outperformed broader utility bond indices. It

should be noted that green bonds may be issued by a variety of companies, including banks. The bonds

reflect their overall credit rating even if the portion devoted to renewable resources is relatively small.

Debt markets’ relatively positive embrace of renewables projects reflects another key element: Issuers

are mostly hedged against declining commodity prices. The vast majority of renewable power projects

have guaranteed pricing for a significant portion of their expected output, either via utility offtake

agreements or from private consumers (e.g. commercial and industrial companies). The same is not

necessarily true of all IPPs, most of which operate assets that consume fuel in their power production.

Those that retain significant amounts of merchant commodity risk do so with the expectation that their

input costs and output prices are correlated and their exposure is to the margin. By contrast, renewable

developer costs are mostly upfront so hedging the output price is essential.

Evidence from commodity markets

Public equity and debt markets provide useful information about the likely funding costs of the three

main types of companies involved in new power generation capacity. But we can leverage other market

data to get a sense of how likely the spot price of their output will hold up in the future. This is relevant

not only to the portion of their future production that isn’t fully fixed but, more importantly, to the

future production of projects that have yet to be financed and built.

If the forward market today for power were severely depressed relative to historical prices, one could

expect more difficult conditions in obtaining either equity or debt financing to proceed with projects.

Notwithstanding pandemic-related delays, there has been a fairly steady rate of development over the

past year and, consequentially, a fairly steady rate of forward power contract selling. But prices have

held up remarkably well. How has this happened?

Natural gas is a significant driver of power prices given its role as fuel in power generation. The decline

of U.S. oil prices this year has resulted in the shutting in of a significant portion of production, not only

of oil but also of associated gas supply. And seasonal factors also now support rising demand as the

northern hemisphere approaches peak winter heating season. So, despite continued economic

weakness, natural gas prices have risen across the forward curve, beyond the current winter peak,

reflecting a more protracted period of tighter fundamentals stemming from lower supply. The chart

below shows January 2022 futures prices as a proxy for the forward curve beyond this winter.

Recent strength in natural gas prices has certainly had a positive impact on forward power prices. Like

any long-dated commodity prices, forward power prices reflect the supply and demand for hedging.

Developers and asset owners need to sell forward in order to secure their financing while consumers

may choose to buy power on a fixed price into the future in order to lock in their expected costs. The

balance of these two activities – rather than actual physical supply and demand in the spot market today

– has the most direct bearing on price levels traded.

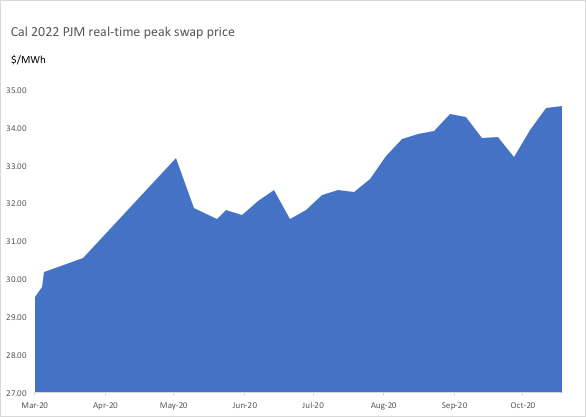

It has been our view that all of the development taking place in the U.S. (and elsewhere) has a

disproportionate impact on forward prices: more forward selling than buying. Indeed, for most of the

past few years this has been the case. But prices have begun to rebound in recent months and this

could can be attributed to the recent strength of natural gas prices. The chart below shows the rebound

of 2022 futures/swap prices in PJM over the past several months.

Conclusion: Implications for financing cost

We have broken out various components within the broader power sector in order to better understand

the financing environment in which they operate. But one aspect of investment is common to all,

whether early-stage development, late-stage operation, or integrated utilities (domestic or foreign):

financing requires a significant degree of commodity price predictability. Ultimately, the availability of

financing depends on the willingness of buyers or financial intermediaries to enter agreements with the

asset owners that fix the price of power for an extended period of time (years). Without that revenue

certainty, financing would be far more expensive to the asset developers and owners.

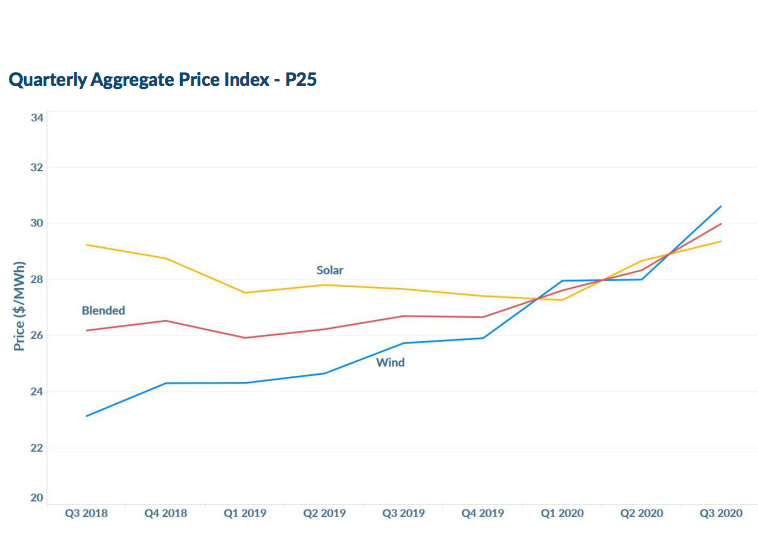

Recent evidence from the power-purchase agreement (PPA) market confirms that the recent strength of

futures prices has translated into higher prices in long-term power agreements. The chart below shows

the recent trend in U.S. PPA price offers (source: LevelTen Energy).

Barring some significant externality, if PPA prices hold at similar levels over the next year – perhaps with

some assistance from firm natural gas prices – then the economics of development are likely to be more

assuredly sufficient to warrant new development. By contrast, a decline in long-term power prices

might limit the willingness of both debt and equity investors to commit capital for new development.

Ultimately, this is the biggest determining factor for the industry’s growth expectations and analysts

should pay attention to long-term PPA levels as well as commodity prices (power and natural gas

futures) in their forecasting of the pace of development.

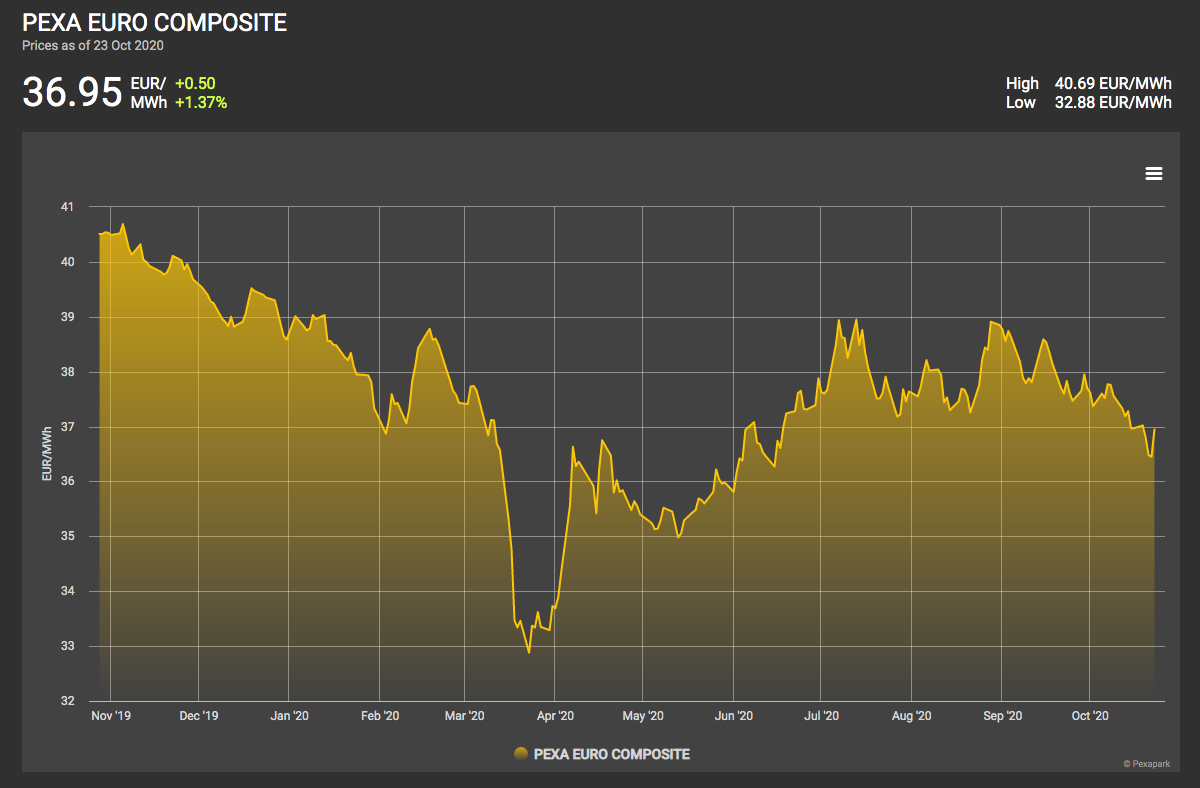

PPAs and power futures have their limitations, of course. There are plenty of examples of financings for

which fixed prices provide only partial reduction of commodity price risk and the remaining portion is

assumed

at higher price levels. This may be evident from the fairly steady pace of financing in Europe

even as PPA prices have fallen in recent months (chart below, source Pexapark).

Development in the U.S. may also find adequate financing options amidst less attractive long-term

pricing, but only to a degree. The continued low cost of most equity and debt capital will allow projects

to move forward at marginally positive economics, but not at negative ones.