Source: NREL, Terms, Trends, and Insights on PV Project Finance in the United States, 2018

Expert advice for every step in your climate journey

Learn moreThis year has been busy for those involved in the U.S. renewable energy industry. Several states have announced targets for reducing carbon emissions or expanded previously established targets. Utilities and independent power producers have clamored to identify ways to participate further in achieving those targets. And then there’s the federal government, which is only beginning to set out the concrete objectives of the new U.S. Administration but which has targets for carbon reduction that are likely to accelerate the recent trend away from thermal generation and toward a greater reliance on renewable assets and energy storage.

Capital markets, meanwhile, have been trumpeting increased interest in climate-related investment vehicles. Banks and investment managers count on steady growth in investments related to ESG (environmental, social, and governance), primarily via equity mutual funds and ETFs (exchange-traded funds). And there are plenty of other, more direct, opportunities for investors to participate in the energy transition, including asset developers and related service providers across generation, storage, and energy-management systems. With a heavy focus on technical innovation and information service providers, venture capital also is ramping up.

Amidst all of the bullish expectations for growth in U.S. renewable generation capacity we wonder on behalf of investors: are the expected returns commensurate with the risk? The question isn’t easy to answer, and only a small portion of research efforts focus on this aspect of development. Academic and other pro-renewable organizations concentrate their efforts on measuring and forecasting assets and their capacities instead of whether or not those assets will live up to their financial expectations. Equity analysts, meanwhile, simply don’t have enough pure-play developers in their coverage to be able to analyze the sector properly on its merits. The most relevant sector – utilities and independent power producers – tends to be clouded either by unrelated regulated activity or by ownership structures that make it difficult to understand the risk and return of new asset development. Research around broader ESG benchmarks, meanwhile, isn’t helpful either as they tend to focus on energy consumers and their reduction of carbon generation, not on developers and producers of energy.

In order to assess the landscape on their own, investors must consider limited information in the public domain (given private ownership of a large number of projects) across a wide variety of regions and pricing terms. This paper builds on previous work (https://alphapoweradvisers.com) providing broad perspective around such an assessment. It also turns the spotlight on an area of infrastructure finance – tax equity – that is not well understood outside the narrow field in which it operates. The state of the tax equity market is very relevant to renewable development today, but as we discuss in a subsequent section it may not be so important in the future.

The underlying investment climate seems accommodating for future renewable development. In addition to a lower cost of equity and most private debt over the past year, there is the prospect that federal legislation will extend existing tax incentives and even expand them, perhaps for a very long time into the future. But accommodating financial conditions and continuing tax subsidies still do not necessarily guarantee positive economics of development projects. From discussions with a number of investors we know that there is enough competition among developers and their financial backers that returns are often driven downward to levels that are questionable for a significant portion of them. Those who fail to win auctions cannot justify the risk versus expected return.

This is not a perspective that one is likely to hear from the legions of analysts who focus only on growth without regard for the investment returns and financial risks associated with construction and operation of renewable assets. Those risks derive from various cost and revenue streams, but tend to be concentrated in the exposure to commodity (energy) price received by the asset in the wholesale market. Since the vast majority of existing projects’ commodity price risk is hedged, market observers tend to discount the likelihood that financial performance might deviate from expectations. But performance can deviate from expectations – in some cases severely.

Measuring risk is, of course, a subjective science and one should never assume that competing firms are using the same metrics. What seems safe to one party could be outside the comfort zone of others, especially when it comes to tail risk. There is perhaps no better example of such risk in power generation than what occurred in the U.S. Midcontinent earlier this year – especially in Texas given the extent of outages and the associated financial liabilities. The true depth of financial obligations is still being worked out and probably will be for some time to come. But it was certainly a big tail event, and there will likely be more such events in the future.

There are many factors to consider in assessing the outlook for financing the renewables industry, among which we focus on a few main themes here:

1) Will traditional tax equity investors, the main source of external equity financing for new renewable generation capacity, continue to drive growth in capacity after several generators suffered significant losses earlier this year? 2) Do those tax equity investors even matter to the overall investment climate, or will other capital providers become more important sources of project financing? 3) How do tax equity and other investors think about the standard practices in use today for managing commodity price risk? Will the methods of hedging against lower energy prices evolve to avoid liabilities such as those incurred earlier this year? And if so, how? Background: Investment climate prior to the February storm

We have characterized various aspects of financial risk in power development among several previous papers over the past year (see References). In general, conditions remained favorable throughout the pandemic, despite initial sharp declines in most measurements of physical activity and the unknowns surrounding a rebound. Improving conditions in broader financial markets, especially in credit, alleviated concerns that developers’ access to project finance would be impaired on a long-term basis.

Evidence from public debt and equity markets continues to reflect a robust desire among investors for exposure to energy assets, especially electric power generation and storage. With a stable cost of capital, the main challenges for developers have been to justify expected long-term returns and to lock down as much commodity-price uncertainty as possible. Fortunately, for the industry, rising long-term power prices in the past year have facilitated the latter challenge. After briefly falling sharply in early 2020, long-dated strip prices for the main liquid hubs bucked the multi-year trend (lower) and appreciated through most of 2020 and early 2021.

The focus on commodity price stability among investors in renewable power generation is largely due to the expansive use of project finance in developing new assets and expanding existing ones. As we’ve noted elsewhere, investors have been more willing to expose themselves to other energy prices – namely, oil and gas – where the obligations tend to be on the balance sheet of owner/operators and where commodity price hedging practices vary considerably and almost never extend more than a few years into the future.

Project finance and associated commodity risk management in power generation development has worked reasonably well over time and certainly helped investors realize steadier returns than they would otherwise have done over several years in which power prices declined, in some cases significantly. The rebound in natural gas and power prices that accompanied the strong resurgence in other asset markets in late 2020 and early 2021 didn’t hurt, either. The rise in prices was sufficiently gradual and steady that it lifted the long-term viability of assets, especially those with merchant tail risk, while not causing undue hedge losses or the associated liquidity issues arising from calls on collateral.

Lastly, the expectation that a new U.S. Administration would turn a friendlier eye toward renewable energy provided yet another source of support to an industry that was already growing steadily. The Biden administration is only now beginning to issue a clearer picture of its vision for facilitating further growth, but for several months the expectation has been building that there would be explicit support for new and existing renewable assets, if only via tax incentives for generation and, potentially, battery storage. Any further mandates that may be introduced into legislation promoting renewable development would be icing on the cake.

It is impossible to overstate the significance of tax incentives to U.S. renewable development over the past decade or so. Tax treatment is a key component of government policy in the U.S. and drives significant activity in other industries as well. For example, tax treatment led to the development of the Master Limited Partnership (MLP) structure, which greatly facilitated the development of pipeline and storage infrastructure in the oil and gas markets. Once established by Congress as a reaction to a perceived need to incentivize investment in a particular area of infrastructure, tax incentives tend to live on indefinitely. Beneficiaries don’t complain and those on the outside often don’t understand the cost of such government programs both directly (government revenue) and indirectly via the skewed impact on allocation of capital resources. As a result, temporary programs tend to become permanent.

The investment tax credit and the production tax credit that apply to solar and wind development, respectively, effectively lower the cost of capital and the required returns of projects, especially in the early portions of their development and productive lives. And they do so in a significant way: the investment tax credit currently is 16% of the total investment cost of a solar project (down from 20% until 2019). The production tax credit is calculated over the life of the project but is also significant in magnitude as it lowers the breakeven cost of production and, hence, the price at which a wind farm can sell in the wholesale market or contract via a power purchase agreement (PPA).

Both tax credits can only be utilized fully if the entity that owns the asset has a tax liability against which to apply it. It is important to note that tax liability is not current, but in the future. As such, it would be risky for a company whose profitability is uncertain to enter into an investment in which performance relies greatly on the company’s steady generation of returns and associated tax liability.

The knowledge system around these tax incentives is highly specialized and limited to those companies that invest in the required legal and accounting resources. Relatively few investors are focused on this niche market aside from banks and insurance companies whose profitability may be volatile but tends to be positive. Their capacity to understand tax law is facilitated by their client business. Manufacturers, by contrast, may not have any reason to look for tax incentives in their business and thus aren’t on the lookout for opportunities to take advantage of them. The fees associated with such specialized knowledge are a significant component of the overall cost of renewable development. They may not rival plant and equipment, but they are certainly greater than for similar investments that don’t require such extensive legal and accounting expertise.

These incentives are distortionary since they have disproportionate attractiveness to some investors vs. others. Perhaps, for this reason, they aren’t used by foreign governments to such an extent; the U.S. is essentially alone among developed economies in its incentivization of business activity via its tax code. Other governments may incentivize development via different mechanisms, including fixed pricing of energy at sufficiently high levels to attract private investment. They may also have carbon pricing schemes that achieve the same goal of raising the price of energy above levels that would otherwise prevail. But those mechanisms do not affect market participants differently based on their unique financial condition.

The tax code’s distortionary impact on market participation and the costs associated with it combine to make this sector ripe for transformation. There is a solid rationale for envisioning an investment landscape in the future that is very different today’s, but a major transformation is unlikely without legislative change in the tax code.

Anyone following the transition of leadership in the U.S. over the past few months will have witnessed plenty of discussion around the importance of clean energy to the new Administration. Although it isn’t clear yet exactly what will end up in any new legislation there is a high likelihood that tax credits will not only remain – they’ll be extended further into the future than they have been in the past. Despite conditioning themselves for the possibility that those subsidies might someday disappear, the vast majority of renewable developers welcome the prospect of their extension given the blanket impact on all participants’ after-tax returns.

If this were the only tax component of new legislation to promote renewable investment the status quo would hold for several more years, and the investor base responsible for the vast majority of new asset development would likely remain distinct from the broader asset base that funds energy development elsewhere in oil and gas extraction, processing and refining. The oil and gas industry has its own government incentives, but it is essential to clarify that those incentives don’t affect companies differently based on their tax situation. As such, those companies tend to finance all of their investment with their capital and credit rating (i.e. on the balance sheet). They may utilize project finance for some large (and relatively predictable) assets, but these tend to be the exception rather than the norm.

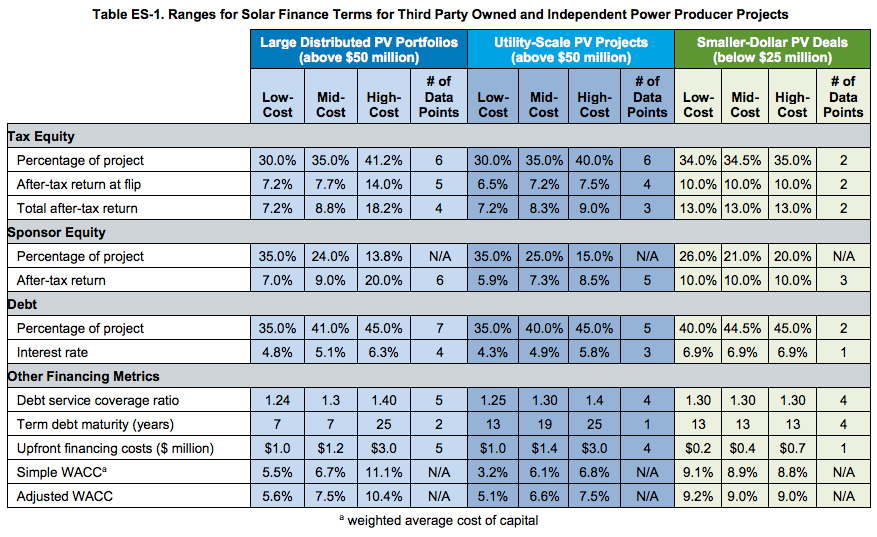

In renewable development, project finance is the norm. And because this involves other investors beyond the main project sponsor, the general structure of capital invested in renewable development is spread among sponsor equity, tax equity, and lenders (table below). This standardized capital structure limits the ability for outsiders to compete with the tax equity sources without either an unusually low cost of capital or financial incentive that is as significant as the tax benefit. While it may seem reasonable to envision a highly talented management team backed by non-tax-advantaged (cash) equity being able to compete against less savvy developers backed by tax equity, in practice the tax benefit is the more significant factor and will generally favor those that utilize it properly.

Source: NREL, Terms, Trends, and Insights on PV Project Finance in the United States, 2018

There are benefits to the existing structure of renewable project finance, including adequate capital availability and designated roles for developers and their financial backers. But there are constraints as well. The passive nature of many tax equity investors means some may lack knowledge around asset operations. Without such understanding, they tend to have less tolerance for risks such as commodity pricing and thus focus on relatively heavy hedge effectiveness. While some such investors have significant experience in this industry and in asset operations, others are in the game for the returns and threats to those returns must be limited wherever possible.

Hedge structures have evolved over time. In the industry’s early years, it was easy enough to guarantee a project’s economics by entering into a long-term physical supply agreement with a utility at a fixed price and no volumetric risk. But with competition driving increasing numbers of developers into the market, the pool of off-takers needed to expand to include non-utility consumers – especially commercial and industrial companies – via corporate power purchase agreements (PPAs). Here, too, the landscape has changed over time: a decade ago such companies behaved like the utilities, agreeing to buy power at long-term fixed prices and in whatever volumes the development produced. More recently, however, competition drove developers to accept somewhat riskier deals. While prices might still be fixed, the tenors were often shorter. In addition, the volumes might also have to be fixed.

It’s impossible for any intermittent generator such as a wind or solar farm to guarantee its production volume. But if competition for long-term buyers drives them to make such a representation, then there are ways to manage it. Developers can put a significant amount of science into forecasting likely production under a range of potential scenarios and only guarantee the portion they feel most confident about. To the extent actual production deviates from forecast, there shouldn’t be any persistent bias; i.e., the errors should balance out over time.

It should be noted that such guarantees are typically contracted via financial agreements, or virtual PPAs, not for actual physical delivery. They are usually structured like financial swaps – settled as a contract for differences versus a published index. Perhaps to make them as much as possible like a physical offtake agreement, contracts for differences in power supply typically reference the hourly or other high-frequency indexes where physical trading occurs. This practice has the benefit of marking an asset’s value against a relevant marker, even if it happens to be a far-off, more liquid trading hub that introduces basis risk to the hedge structure. But marking to a physical index certainly has downside, especially to the developer during periods of unforeseen volatility.

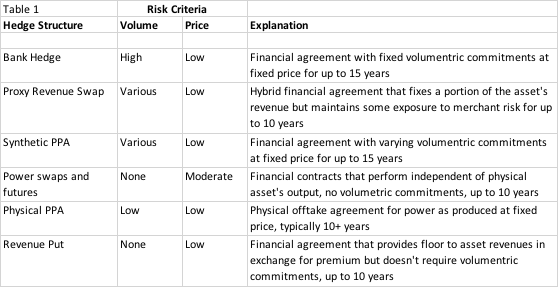

For the most part, these various hedge agreements have done their job well. Most have protected developers, operators, and – importantly – their investors against declining commodity prices while also providing energy consumers with the opportunity to take the other side (hedge against rising prices). While actual production volumes and spot-market pricing may deviate from asset owners’ long-term projections, PPAs and other hedge structures tend to balance the physical activity in a way that greatly lowers the volatility of monthly revenues. Different structures cover risks in various ways (table below) but all provide some degree of stability to financial performance most of the time.

There is some concern that tax equity supply is more constrained today than in the recent past. This is partly due to losses sustained by a number of asset owners in Texas this year, which we address below, but for other reasons as well, including lower tax liability among U.S. corporations since the 2017 federal tax reform. In our view, any assessment of the availability of financing must be considered on a spectrum as investor interest is always present at a specific price and relative to perceived risk. That price may be higher today for some projects but is governed by competition, not only among traditional tax equity investors but indeed among a broader pool of investors that could absorb waning interest among the traditional players.

Among all of the factors that will drive changes in U.S. generation capacity, we have tended to focus on the financial ones. In previous papers we questioned whether there will be sufficient demand from end- users to purchase all of the PPAs that will be required by developers to guarantee their output. The answer to that question, of course, also depends on the price. In the case of financing, the clearing price is the clearing return on capital as financing ebbs and flows based on the industry’s ability to produce returns. Looking at the past several years, returns appear to have declined to reflect additional capacity and greater competitiveness among developers, especially in markets such as ERCOT with low barriers to entry.

Such a shift in returns isn’t evident from assessments by industry analysts, government agencies or academic institutions. This assessment is based on discussions with a limited number of market participants and is not drawn from an exhaustive survey of representative data. Indeed, given the private nature of most such investments, there is no such data repository. The closest evidence from public markets is the very narrow industry of so-called yield companies which own and operate generation assets but only after they have been built. Thus, yield companies don’t represent the development stage of investment which has considerably higher risk and expected return. They are far more predictable in their operations but we can still utilize their experience to get a better sense of how returns might be changing over time for earlier-stage companies (developers).

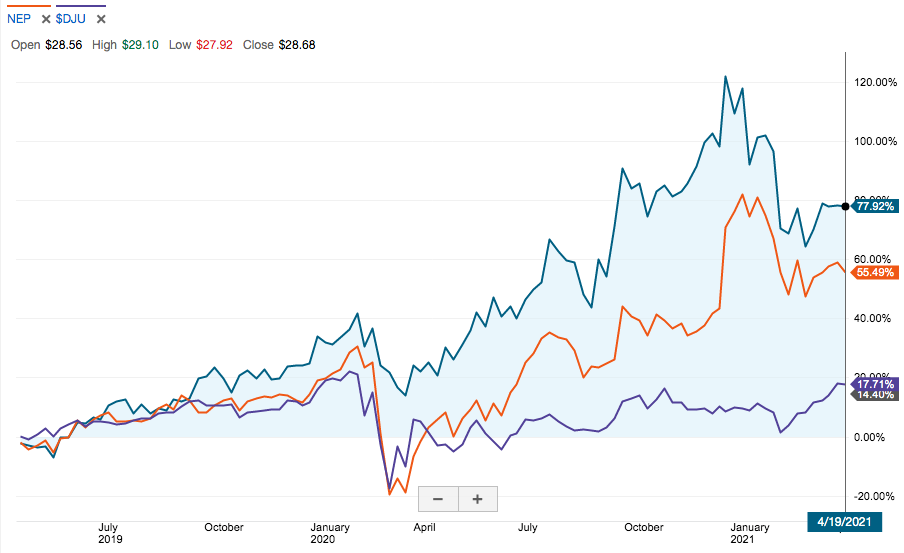

Three representative yield companies focused on North American renewables are Clearway Energy (once part of NRG); NextEra Energy Partners (NEP), a publicly traded entity under the NextEra Energy (NEE) group of companies; and Pattern Energy, which was taken private about a year ago. Both Clearway and NEP are highly dependent on sourcing new assets from developers that have built and begun to operate assets and then seek to sell those assets in order to move on to their next projects. In the case of Nextera Energy Partners, the vast majority of their holdings are supplied by an affiliated company, NextEra Energy Resources (NEER). Clearway Energy sources its assets from other developers. The chart below shows the equity performance of Clearway (turquoise) vs. NEP (orange) and the DJ utilities index (purple) over the past two years.

The prices that yield companies pay for asset investments should reflect the overall market for renewable generating assets and the environment in which developers are also competing. Clearway and NEP are generally viewed positively by equity analysts and considered market outperformers. Their equity prices have outperformed broader market benchmarks over the past year and significantly outperformed utility sub-indices. But those analyst recommendations and stock price appreciation hinge on growth in companies’ assets as opposed to expected returns from existing assets. Profitability in 2019 and 2020 was negligible or negative net of interest expense, which is considerable for both companies given their relatively leveraged capital structure (another reason to be highly hedged on commodity price exposure). While they may be investing in new assets with target returns closer to 10% – especially on a levered basis – their actual returns to shareholders were considerably lower over the past couple of years.

Financing costs didn’t increase during this period. If anything, they have gotten cheaper. So under- performance can only be attributed to operations, either income and expense, as well as some true externalities such as the bankruptcy of their offtakers. It doesn’t matter to us where any particular asset owner might underperform; what matters is more generally that they may not have fully realized the expected returns on assets they purchased. This would be consistent with rising competition among the many privately-owned asset owners in the renewables space.

This doesn’t necessarily imply that such companies are overvalued; the growth story is certainly compelling for investors. But growth has implications for long-term commodity pricing which, in turn, affects the industry’s ability to generate returns – a topic we have covered at length in a previous paper. More importantly, if the experience of long-term asset owners is one of skinnier margins then it stands to reason that the same dynamic ought to be affecting asset developers. Investors must accept lower returns for a given level of risk.

Another way to gauge the returns on equity for renewable developers is via the limited information published by investors themselves. The handful of large banks and insurance companies that provide most of the equity capital tend to be public corporations with obligations to disclose this information. But it isn’t easy to identify, as its scale is a rounding error relative to their overall operations (a collective $15-$20 billion per year out of trillions of dollars of capital raised and provided). The banks don’t trumpet the performance of this part of their business, and what we can observe suggests that tax equity investments tend to produce modestly positive returns and some negative ones – somewhat in line with the performance of the yield companies in 2019 and 2020.

To recap, over the past couple of years there has been some evidence that returns were declining for investors in the development and operation of renewable power assets. This is consistent with our overall view that renewable capacity cannot continue growing rapidly without a commensurate impact on project economics unless there is some compensating decline in capacity from other sources. While there has been a continued decline in capacity from carbon-based generation, it hasn’t been fully compensatory. U.S. generation capacity is rising faster than demand and reserve margins are risking, especially outside of Texas.

Plenty has been written about the severe impact that winter storm Uri had on energy production during one fateful week of February 2021. The effects were felt throughout the U.S. Midcontinent in oil and gas production and transportation and, especially, electric power generation in Texas. The pricing structure of the ERCOT market contributed significantly to the financial liabilities that occurred over the course of the week. Total liabilities across various market participants could exceed $100 billion once all of the obligations are disclosed.

The ERCOT market structure is simple enough and is meant to incentivize new capacity by providing the opportunity to receive extraordinary returns at times of peak demand – typically during the hottest days of summer. Texas has eschewed the establishment of a capacity market to facilitate additional generation capacity and instead leaned on the potential for highly remunerative energy markets to provide that incentive. The market structure didn’t foresee generators’ inability to operate when prices are highest, especially in winter. It hadn’t happened many times before and certainly not for the duration that occurred earlier this year.

The February storm and its severe impact on prices of power and natural gas had varying effects on power generators, depending on their hedge structures. There was significant variation even among those that hedged via financial commitments to produce stated quantities. If they could generate during the high-price period they were likely paid the low, long-term rate for the contracted volume. But if they couldn’t generate they needed to make up the volume by buying on the spot market (high) and selling at the long-term price (low). Only if they were able to generate above their long-term committed volume would such a generator have been able to benefit from the high spot-market price by selling the excess power into the spot market (assuming the buyers ultimately honored their purchases).

Others that hedged via more lenient structures allowing them to sell whatever they could produce (at a fixed price) were not on the hook for anything. For any power generator operating under a long-term contract “as produced” – i.e., with no volumetric obligation – the price volatility was not relevant. If they were able to generate during the high-price period, they were likely paid the same low fixed rate they had agreed to in their long-term contract. If they couldn’t generate, they had no financial obligation to do so.

Unfortunately, for many, the former hedge structure seemed safe enough – until it wasn’t. It seemed safe because it priced off a recognizable index at a volume that was commensurate with their asset, assuming reasonably normal weather conditions. Pricing off a physical index didn’t seem a big risk because it had not previously held at such a high level for several days on end. But now it is clear that it was a significant risk and remains so as long as there is still potential for equipment to freeze and power prices to rise significantly from widespread shortages in generation.

Given the prevalence – especially in recent years – of fixed-volume offtake agreements, there is a high likelihood that several independent generators have significant liability from the winter storm. The severity of the price moves and its unprecedented length in effect (five days) was such that obligations for generators under fixed-volume agreements that couldn’t run might have been on the hook for a year’s returns or more. For owners that had considered their assets’ long-term hedges to be highly effective in reducing commodity price risk, such losses exposed the deficiencies of fixed-volume contracts in stress scenarios. Such scenarios would surely be considered to be more likely going forward

– contributing to an overall reassessment of risk that would alter financial models significantly. The impact of winter Storm Uri has yet to be fully realized and could drag on for a while. But the cost to some asset owners might be sufficient to drive their investors away from the industry if they weren’t already doing so based on declining returns before the storm. If tax equity investors were to back off, then the cost of capital for developers would rise commensurately, pressuring returns on their investments. This has probably already begun, and the real question is one of degree.

There is, of course, no restriction on other investors taking the place of tax equity investors in financing new development. Any pool of capital can compete for development opportunities in any jurisdiction. Importantly, they can – and should – take advantage of the tax credits that would be available to them from such an investment, just like tax equity investors do.

If the returns were to justify the risk there should be plenty of non-traditional (tax equity) investor interest in joining the renewable space. The question is: do they know how to? As discussed above, tax law requires specialized knowledge. Investors coming into this space for the first time need to invest in legal and tax resources to better understand the benefits and risks of doing so.

These costs could be shared more efficiently across various investors if they are coordinated by aggregators whose role is to pool investment resources. Aggregators can streamline the process and spread the incentives and risk among various participants. Indeed, this is a role suited perfectly to the banks and securities firms that have typically provided such financing directly. The only restriction should be on the individual investors having sufficient tax liability to utilize the credits.

There is potential for non-traditional investors to become more involved in renewable development even without obtaining a deeper knowledge of tax law. The new U.S. Administration is considering making the tax benefit less exclusive to only those businesses and individuals with a consistent tax liability. They could institute so-called refundability, also known as direct pay, which means that the tax credit is not applied to a future liability (as it is currently) but rather is simply paid by the U.S. government whether or not the owner has a liability. This would effectively eliminate the distinction between tax equity investors and all other investors in these projects.

It’s still too early to handicap the likelihood of such an outcome with any confidence, but such an outcome is certainly possible in the year ahead. If it comes to pass, this change would certainly increase competition for projects. It would introduce broad swaths of institutional investors to an asset class from which they previously were disadvantaged. For some, it could be attractive not only for potential returns and portfolio diversification but also for participating more directly in an industry that checks important boxes for investing under ESG guidelines. Renewable power development covers them especially well.

To date, active ESG investors have tended to focus on owning companies that are either cutting their direct carbon footprint or demanding that their suppliers do the same. As such, the supercharged ESG investment world reduces carbon, but does not take the more active approach to developing competing resources. Equity capital in the ESG sphere is cheap and getting cheaper, and if those investors were to suddenly be on a level playing field with investors that have traditionally been involved in renewable development the field could open up significantly.

There’s another potential source of investment that could come about from changes in tax legislation. Currently, investor-owned utilities are disadvantaged in their investment in renewable assets – especially solar – because they aren’t allowed to utilize the investment tax credit in the same way that non-utilities can. Rather than realizing that benefit in the first year, as other investors do, investor- owned utilities must spread it over the entire life of an asset. While they might eventually realize the benefit decades later, this difference makes them uncompetitive in the current allocation of resources.

A change in this aspect of tax law could even the playing field further. But it should be noted that the investor-owned utility industry would approach such investments differently from all of the other types of owners of current and future renewable generation, including tax equity investors, institutional investors, and industrial companies. Regulated utilities wouldn’t have to hedge the commodity price. Rather, they could simply charge their customers a negotiated price for their output, subject to their local commission’s approval. As such, this is the one potential investor group that wouldn’t have to worry about achieving targeted returns for a given level of risk. It would be more or less guaranteed.

In addition to institutional investors and, potentially, investor-owned utilities, there’s a whole slew of companies that also have little or no experience in renewable asset investing but which also could be interested in participating in future development. There have been a variety of responses among oil and gas companies to the shifting preferences of equity investors in the energy space – away from those companies involved in the production, processing, and distribution of carbon-based energy sources, toward those that are focused on renewable sources and non-emitting energy storage systems.

Most traditional oil and gas companies have embraced the investor challenge, making direct investments in green technology and vowing to shift their output toward more sustainable sources over time. Some have even committed to carbon neutrality over the course of years or, more likely, decades. Others, meanwhile, have made no firm commitments.

To our knowledge, no oil and gas company has yet announced any passive investment in renewable resources. This sort of thing isn’t in their DNA. Energy producers bring technical and logistical experience to the world’s energy challenges – not investment capital, which their investors provide. But large energy producers have significant resource development plans – some of which are now being redirected toward renewable capital projects, including power generation, energy storage, carbon sequestration, and hydrogen production. Arguably, a small portion of those funds might be directed toward other developers, if only as an intermediate step toward making their own, more direct, investments further down the road.

This is possible today, with or without any change in the existing tax structure. Any oil and gas company, refiner or midstream processor – or coal miner, for that matter – could expect to benefit from the tax credits offered by investing in renewable developments as long as they have sufficient tax liability to which to apply it. They might need to hedge their production somewhat more than they otherwise would to maximize the likelihood of positive net earnings (and, thus, income tax liability). But there isn’t anything in the federal tax code that would put such companies in a competitively disadvantaged position versus traditional (financial) tax equity investors.

Indeed, given the knowledge transfer of such direct investing, arguably such an investment should have relatively greater value to an energy company considering a long-term strategic shift than it has to a bank that has less interest in understanding the business of renewable generation and instead is more focused on returns and being recognized for green investment. In this sense, such investment by a traditional energy company would represent more of a true partnership of interests.

Of course, any changes in tax law such as refundability (direct pay) that even the playing field could also incentivize oil and gas companies to allocate resources to renewable power generation. They wouldn’t have to worry about having adequate tax liability as they currently do, so they would be more at liberty to be exposed to commodity pricing in their primary business.

As discussed above, limiting commodity price risk is a hallmark trait of tax equity investors and debt providers to renewable projects. They want to make sure that the expected returns are relatively certain. Such hedges may be structured in a way that gives those investors a false sense of security, but in general they will continue to demand that developers find long-term buyers for their output at some relatively certain price.

Any new types of investors that might come into this market may have a very different set of requirements for risk management, including some that aren’t so focused on guaranteed returns. After all, institutional investors don’t hedge commodity price risk in many of their other holdings. We’ve discussed at length in previous papers the key distinctions between investors in power vs. other energy markets such as oil and gas and found that the risk profiles differ markedly. But if the investment pool for renewable assets were to broaden to include participants from areas that aren’t as risk-averse, then the hedging profile for renewable assets could become less rigid.

There might be another factor at work in reducing the very high hedge effectiveness of most renewable projects. In addition to the potential for new investor participation noted above, even those that have historically been active in this space might consider doing things differently in the future. This would only come about from such a significant – and painful experience with fixed-volume hedges such as occurred earlier this year.

How can investors seeking steady returns lessen the risk of their hedges blowing up on them? They can choose a hedge structure that isn’t as effective (i.e., one that doesn’t offset the physical market price as dynamically) but also doesn’t subject the investor to a shortage such as occurred in February. In other words, by using a blunter instrument: something that protects against a broad decline in wholesale power prices but doesn’t penalize for lack of production.

There are plenty of candidates for such a hedge. As in everything, there are structures that provide lots of optionality at high cost. And there are structures that provide relatively little benefit at comparatively low cost. There are no free lunches; nor are there any clear choices based on risk versus return. The spectrum is fairly continuous.

Consider the range of options, starting with the most expensive. Some market analysts have called for developers to embrace more of an options-based hedging profile in the wake of recent events. Some put options can be simple, such as those that are settled against the simple spot-market price for a given volume. Others are more bespoke, such as those that combine price and volume to guarantee a specified revenue to the developer. It might be compelling to consider having a hedge that only pays the developer in low-price circumstances but doesn’t require any additional compensation in high- priced ones. But such solutions have a price: the option premium. And the greater the specialization the higher the price. As a result, options have historically had a limited role in the development of renewable generation and, if anything, the experience from February makes options even more expensive than they were previously. The flexibility they bring to the developer will surely cost enough to significantly affect the project’s economics. This is especially true given the long-term nature of hedges and the importance of time value to option prices.

A simple, and cheaper, solution would be to stay with something that behaves like a long-term swap – as PPAs, VPPAs, and bank hedges do – but which settles off an index that is less variable than the hourly or other intraday spot price. Oil and gas developers have long utilized hedges that price against monthly indices. They may sell their physical production against more volatile spot indices but hedge in more garden-variety futures contracts (or swaps priced off futures) that are transparent, liquid, and easy to implement. Correlations between spot and futures are reasonably high – depending on the market – and they can be sufficient to give owners the confidence that their operations are hedged against a broad decline in commodity prices. We propose a representative structure in the Appendix below.

We have described the climate for equity investment in renewable power development through a slightly different lens than in previous papers. Our focus on tax equity is based on its historical significance to U.S. renewables development, as well as the perception that investors’ risk tolerance might be in decline in the aftermath of this winter’s storm and its impact on financial settlements in the wholesale power market.

We believe that there is plenty of equity capital available among traditional sources. However, we question the underlying assumption that tax equity investors are consequential to the pace of development. There are other investors out there who might participate actively if they knew how to exploit the unique tax benefits of investing in renewables. Those knowledge systems are specialized, but they are by no means limited to the banks and financial firms that have dominated the space until now. Other investors might eagerly jump into the market if the opportunities were sufficiently attractive, figuring out how to extract those tax benefits in ways they may never have previously considered. Banks can help them gain that understanding.

As the U.S. Administration pushes for additional investment in renewable generation and storage and are cheered on by universities, think tanks, and other research organizations, it is important always to understand the attractiveness of such investments from the equity owner’s perspective. A broader population of equity providers might fill the ranks over the next several years, especially if tax law changes level the playing field. But if returns don’t warrant the risks, all of those organizations’ bullish growth projections will need to be amended.

Finally, we address the risk tolerance of all investors and the rigid hedging policies that have dominated renewable development project finance over the past several years. We question the importance of structuring hedges on physical market indices and introduce the case for simpler hedges – with associated lower effectiveness. Such hedges wouldn’t offset all of the price declines that today’s hedges do, but they come with a significantly lower cost than option-based alternatives and with far lower tail risk that many existing hedges exposed last February. If investors are willing to live with somewhat greater uncertainty during normal times, they should be able to avoid some unexpected losses during unusual weather events.

We propose a simpler hedge for renewable developers to consider. As outlined above in Table 1, there is a wide variety of energy price hedges that developers and consumers may enter for 10 years or more. Various structures incorporate different options and obligations, but any of them that is financially settled must reference a price index as the basis for their settlement. Most often, that reference price is a spot market index – typically real-time – incorporating peak, off-peak, or round-the-clock periods within any given day.

The index is typically chosen to mirror most closely the asset’s actual exposure in the physical market. Any financially-settled hedge is expected to have cash flows that offset the impact of price changes on the asset’s returns. Combining the asset’s performance and the hedge should render relatively flat revenue over time. Hedge effectiveness, or the degree to which the hedge offsets the physical market return, is a key metric on which investors depend to quantify their confidence in revenue forecasts.

High hedge effectiveness improves forecast confidence. But it comes with associated costs. First, the most effective hedges are often settled against indices for which there is relatively limited market pricing. This is especially true of illiquid nodes, outside of the trading hubs. Such illiquidity tends to be reflected in a lower long-term price at which counterparties are willing to bid for a long-term financial hedge such as a VPPA. For this reason, hedgers tend to avoid them and opt for the more liquid hub benchmarks even if doing so lessens hedge effectiveness by introducing regional basis risk between the node and the hub.

Next, hedges tend to be settled on hourly or other intraday pricing. Wholesale power prices can vary significantly over the course of a day, especially between peak periods and off-peak periods. Both buyers (power consumers) and sellers (asset owners) are exposed to intraday pricing in their physical business and seek hedges that most effectively offset such price volatility. As discussed above, hedge effectiveness has its virtues but also can have significant costs if the asset isn’t producing when prices are at their highest but is still expected to settle as if it were producing.

We propose that such asset owners with long-term financially-settled agreements consider a less effective hedge if they are required to settle against a fixed volume even when their asset isn’t operating. If the main goal is to hedge against lower energy prices, then they don’t need particularly stringent hedge effectiveness given the risk associated with it.

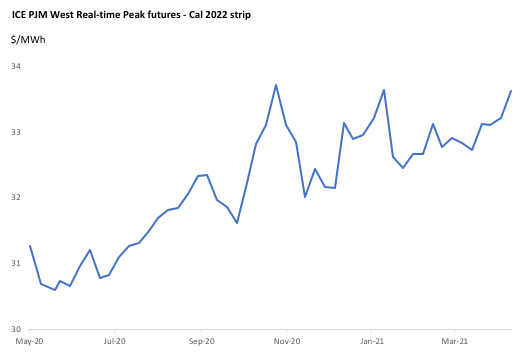

Futures contracts provide an alternative to spot-market indexes, and Intercontinental Exchange (ICE) futures are the most liquid and relevant to U.S. power prices across the main trading hubs. Futures reflect a full month of physical market pricing, so a hedge against the first-nearby futures contact would have a very similar effect as a hedge against the physical market. But if the hedge were instead settled off the second-nearby contract (i.e. one that is a month further into the future), then settlement would take place against a contract that expires before it begins to reflect physical market prices.

Over long periods of time, futures prices of the same commodity and location tend to have high correlation across various expirations. So, a broad rally or decline in prices should be reflected throughout the forward curve. To the extent that such correlations hold, then hedges placed anywhere on the forward curve have some effectiveness.

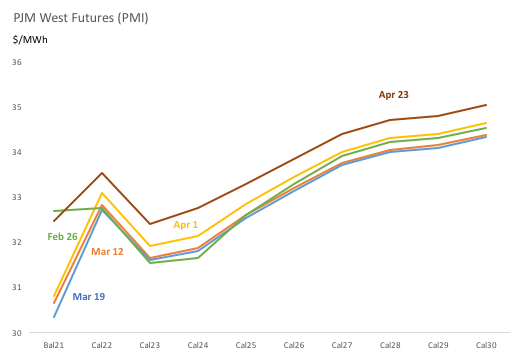

The chart below shows changes in the forward curve for PJM Western Hub Real-Time Peak (PMI contract) at weekly intervals over the past couple of months. A strip of futures representing spot- contract power prices over the next 10 years would be nearly identical to a strip of futures representing the second-nearby contract. Where they tend to diverge is in the front of the curve, as those monthly contracts roll off. If the main purpose of the hedge is to offset a broad decline in prices (e.g. below $30/MWh), then both structures will provide a significant degree of protection. The strip of spot-month futures will be more effective in hedging a physical asset, but the alternative structure has somewhat lower volatility.

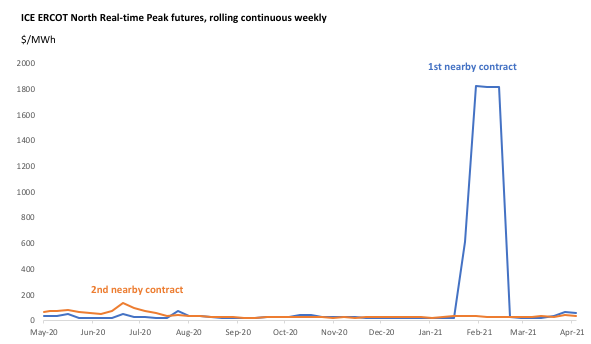

To illustrate, consider the February 2021 contract on ERCOT North Hub Real-time Peak (ERN), which expired in early March 2021 at $1818/MWh (reflecting the high prices during the week of February 15, combined with the lower prices during the rest of the month in which it was the prompt contract). A developer settling a PPA against this contract would have experienced a similar exposure as a developer that hedged against a ratable volume of physical market prices.

The January 2021 contract expired a month earlier, in early January, in the low $20s/ MWh, as did previous monthly futures contracts through late 2020. Importantly, even after the February event, the March 2021 contract traded back down to below $25/ MWh by the time it expired. So, in this example a developer could have hedged February physical production against the expiration of the January contract (and hedged all other months in a similar fashion). The settlement could be against the last day (expiration of the futures contract), as is most commonly done, or it could be against the average of the daily settlements of the January contract during a different interval of time prior to expiration. The fixed price portion of the swap or VPPA would be denominated as it usually is – in $/ MWh determined at the beginning of the contract.

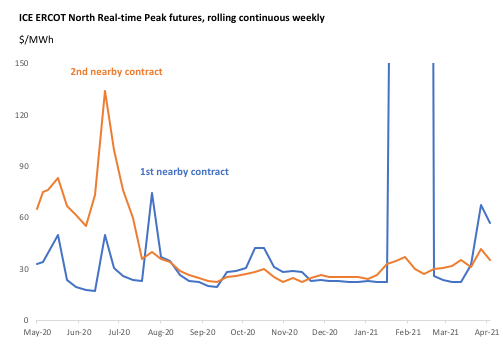

This alternative hedge would likely have less effectiveness and lower volatility during most of the year than a hedge against the first-nearby contract. But the second-nearby contract isn’t always less volatile. Last summer, for example, the futures market reflected tighter fundamentals in midsummer than what eventually came to pass. The charts below show the market’s anticipation, especially during early July, when the August contract rallied above $120 while July futures prices remained around $50. The first chart is intentionally scaled to reflect somewhat normal market conditions. However, the second chart is the more accurate one, scaled to accurately reflect the market during winter storm Uri when first- nearby prices completely dislocated from the rest of the forward curve.

A developer utilizing either of these hedge indexes would benefit from protection against the lower price over the long term. They are both effective, though to varying degrees. Hedging via the first- nearby contract is the more effective hedge, and for this reason is almost exclusively chosen as superior despite the risk of plant outages and the potential need to cover contracted volumes. Such episodes point up the merits of considering an alternative hedge in a slightly deferred contract.

Capacity growth and its potential impact on energy prices and asset values, February 2021. https://img1.wsimg.com/blobby/go/289b2c0f-04e5-4164-b8f52f17850f3b7a/downloads/Power%20Risk%20Feb21.pdf?ver=1618843318726

Assessing the investment climate for new generation/storage, October 2020. https://img1.wsimg.com/blobby/go/289b2c0f-04e5-4164-b8f52f17850f3b7a/downloads/Power%20Risk%20Oct20.pdf?ver=1618843318852

A potential role for investors in long-term power contracts, May 2020. https://img1.wsimg.com/blobby/go/289b2c0f-04e5-4164-b8f52f17850f3b7a/downloads/Power%20Risk%20May20.pdf?ver=1618843318884

Copyright © 2025 Tellus Markets Corporation